Types of Income Tax

Income tax in India is classified based on the nature of income:

- Income from Salary: Earnings from employment, including basic pay, allowances, and perquisites.

- Income from House Property: Rental income from owned property.

- Income from Business or Profession: Profits from business or professional practices.

- Income from Capital Gains: Earnings from the sale of capital assets like property, stocks, or mutual funds.

- Income from Other Sources: Residual income such as interest, dividends, or winnings from lotteries.

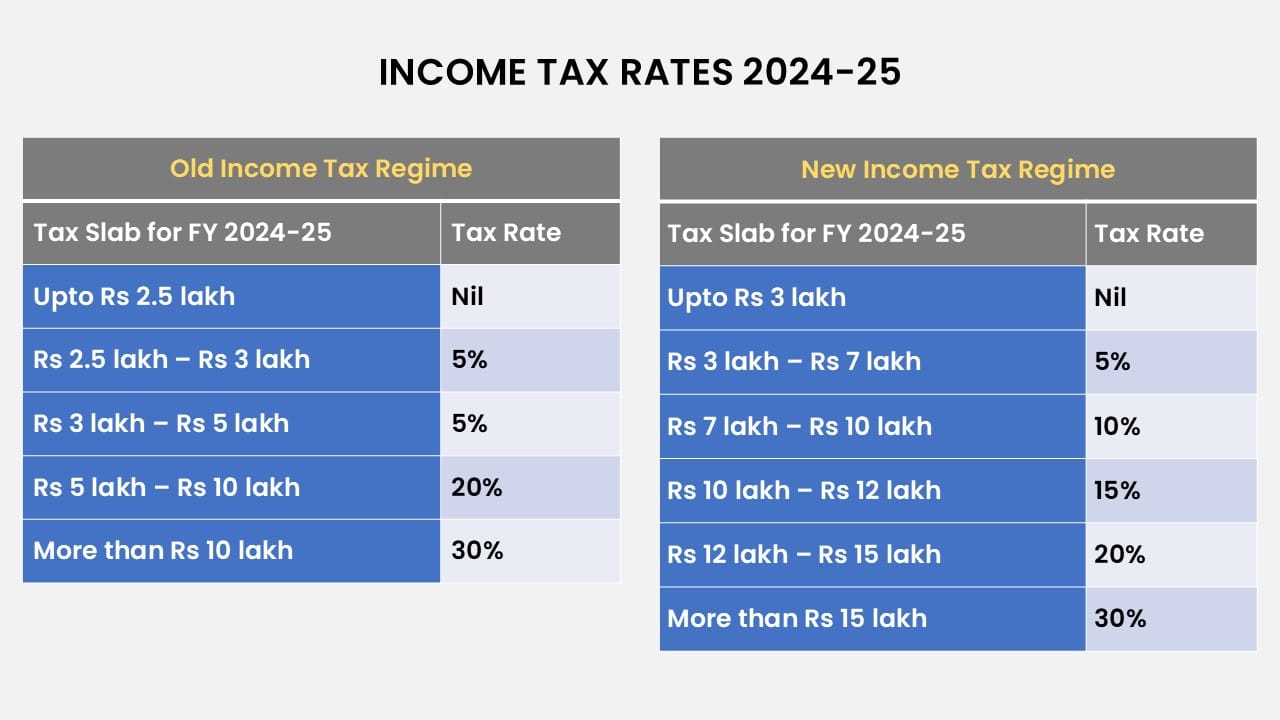

Choosing Between Old and New Regime

Choosing the right tax regime depends on your financial situation like sources of income, types of investments, and more. If you have significant deductions and investments, the old regime may be more beneficial. However, if you prefer lower tax rates and simplified compliance, the new regime could be advantageous. Here’s a comparative analysis:

Old Regime

Pros

- Allows for various deductions and exemptions.

- Beneficial for taxpayers with high investments in eligible schemes.

Cons

- Higher tax rates compared to the new regime.

- Requires meticulous record-keeping and documentation for claiming deductions.

New Regime

Pros

- Lower tax rates.

- Simplified tax calculation and filing process.

Cons

- Does not allow for most deductions and exemptions.

- May not be beneficial for taxpayers with significant eligible investments.

Income Tax Returns (ITR)

Income Tax Return (ITR) is an annual filing of income details to the Income Tax Department, Ministry of Finance, GoI. Every taxpayer should report their income, expenses, deductions, investments, and taxes paid. It is a mandated activity for all individuals who earn income above a certain threshold.

The ITR form includes details of income from various sources such as salary, business profits, property rental, capital gains, and other sources. It also accounts for tax-saving investments and deductions under various sections of the Income Tax Act, which help reduce taxable income. After assessing the total tax liability, if the taxpayer has paid more tax than what is due, they can claim a refund; if less, they need to pay the balance.

Filing an ITR is important as it serves as proof of income, is required for processing loans, visa applications, and other financial matters, and ensures compliance with tax laws, avoiding penalties and legal issues.

Filing ITR (Income Tax Return)

Filing on Income Tax Returns (ITR) must be done on or before 31st July of every year for the previous financial year (Assessment Year). ITR Returns be filed in both online and offline modes. While online filing is the most recommended process for simplified filing, offline filing requires the support of a certified chartered accountant (CA). Offline mode is preferred by taxpayers with high incomes and diversified investments and liabilities.

How is Income Tax Paid to the Government of India?

Income tax in India is paid to the government through three primary methods:

- Tax Collected at Source (TCS)

- Tax Deducted at Source (TDS)

- Self-Assessment Tax

Here’s how each works:

Tax Collected at Source (TCS)

Certain sellers collect tax at the source itself when specific transactions occur. For example, when you purchase goods like alcohol, tendu leaves, or minerals, the seller collects tax at a specified rate. This TCS is then deposited with the government on your behalf. The amount collected is later reflected in your tax credit statement (Form 26AS) and can be adjusted against your total tax liability.

Tax Deducted at Source (TDS)

TDS is a method where tax is deducted directly from your income by the payer before it reaches you. Common examples include salary, interest from banks, rent, and professional fees. The deducted amount is then deposited with the government, and you receive the net amount. The deducted tax is reflected in Form 26AS while filing annual returns and helps reduce your overall tax liability.

Self-Assessment

After accounting for TDS and TCS, if any additional tax liability remains, it must be paid by the taxpayer through self-assessment. This is typically done while filing your income tax return. Self-assessment tax ensures that the taxpayer has paid the full amount of tax due for the financial year.

These methods ensure the efficient collection of income tax in India.

Conclusion

Understanding income tax is essential for every earning individual. It not only ensures compliance with legal obligations but also helps in effective financial planning and tax optimization. By leveraging the available deductions and exemptions, taxpayers can significantly reduce their tax liabilities.

Frequently Asked Questions (FAQs)